Table of Contents

Introduction

Is DISH becoming an Amazon-backed wireless carrier, or is that headline missing the real story?

Recent coverage around DISH Network and Amazon has fueled speculation that Amazon is preparing to enter the wireless carrier market. The assumption is simple: Amazon powers DISH’s 5G network, sells its plans, and could eventually disrupt telecom the way it disrupted retail and cloud computing.

That assumption is wrong.

Amazon is not positioning itself to become a wireless carrier. It is positioning itself to profit from the weaknesses of wireless carriers—without owning spectrum, radios, or regulatory risk.

This article explains what the DISH Amazon wireless carrier narrative gets wrong, how control and money actually flow between the two companies, and why Amazon may already be winning in wireless without ever operating a network.

This is not a consumer explainer. It is an operator-level breakdown of incentives, economics, and long-term leverage.

The Myth of “Entering Wireless”

Becoming a wireless carrier is not a branding exercise. It is a commitment to:

-

Spectrum auctions and long-term licenses

-

Regulatory exposure (FCC compliance, emergency services, lawful intercept)

-

Physical infrastructure (towers, radios, power, backhaul)

-

Device certification cycles and OEM negotiations

-

High churn sensitivity and politically constrained pricing

These are fixed, compounding liabilities—the kind of exposure Amazon has generally steered away from.

Amazon’s core businesses tend to optimize for:

- Variable cost structures

- Contractual leverage

- Optionality to exit or renegotiate

- Owning a carrier appears to fail all three tests.

This helps explain why Amazon does not own airlines, railroads, or last‑mile telecom infrastructure—even though it touches all of them.

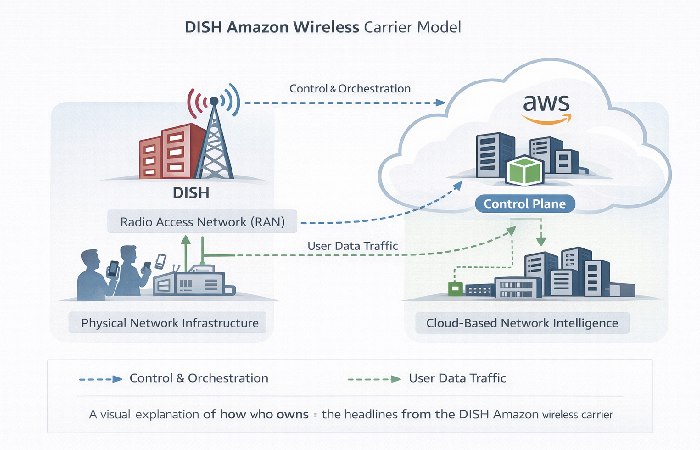

Amazon’s Actual Position: Infrastructure Landlord

To understand the relationship, you must separate control planes from risk planes.

DISH operates radios, spectrum, and customer liability.

Amazon controls two upstream choke points:

-

Cloud infrastructure via Amazon Web Services

-

Customer acquisition via Amazon’s retail ecosystem

Neither role exposes Amazon to coverage complaints, churn spikes, or regulatory penalties. Both roles scale revenue as traffic grows.

This is not partnership symmetry. It is structural leverage.

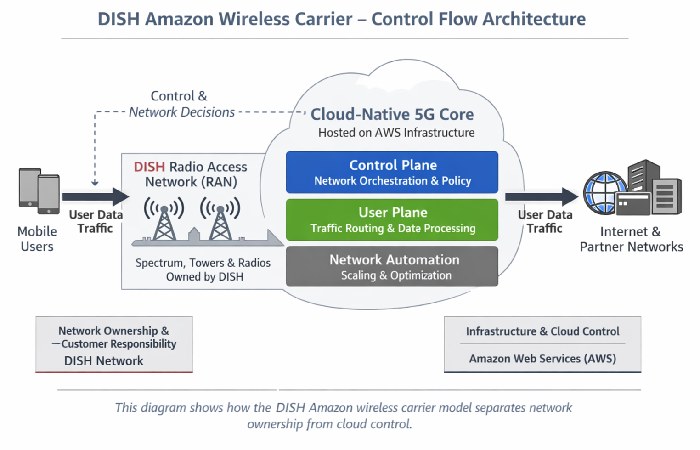

Control Flow: Who Owns the Network Brain?

DISH’s network is frequently described as “cloud-native,” but that phrase hides a critical operational shift:

-

Core network logic

-

Network orchestration

-

Scaling and automation

…run on AWS infrastructure.

That means the decision-making brain of the network sits on infrastructure owned by Amazon, not DISH.

At low scale, this is an advantage:

-

Faster iteration

-

Lower upfront CAPEX

-

Easier automation

At national scale, it becomes dependency:

-

Compute costs scale with traffic

-

Optimization is bounded by cloud pricing

-

Exit costs increase over time

Cloud-native reduces entry friction, not operating gravity.

Distribution Is Not Ownership

Selling wireless plans on Amazon is often portrayed as disruptive. Operationally, it is much narrower.

Amazon controls:

-

Discovery

-

Checkout

-

Promotions

DISH controls:

-

Network performance

-

Customer support

-

Billing disputes

-

Churn management

If service quality dips, formal regulatory and network liability sits with DISH, not Amazon, even though some customer frustration may still spill over onto Amazon’s brand and marketplace policies.

If margins compress, Amazon’s commissions are contractually protected in the short term, but any severe or prolonged pressure on DISH would also threaten Amazon’s long‑run revenue from the relationship.

This is top-of-funnel monetization, not lifecycle responsibility.

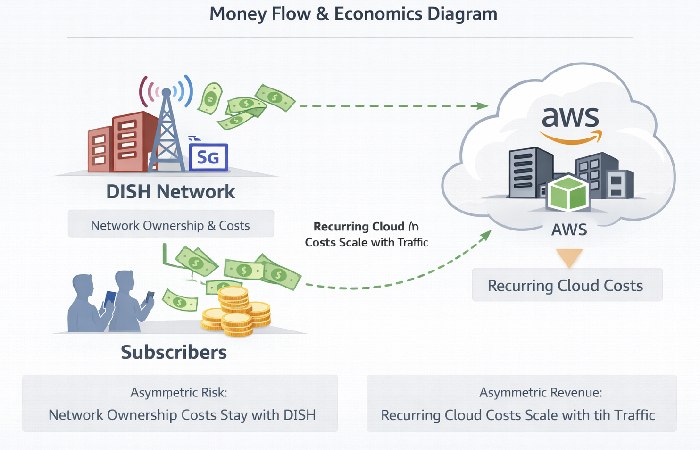

Money Flow: Who Gets Paid First?

Follow the money, not the headlines.

As subscriber traffic grows:

-

AWS compute and storage usage rises

-

Cloud spend increases automatically

-

Amazon’s revenue scales without incremental regulatory exposure

Meanwhile, DISH must:

-

Absorb spectrum costs

-

Maintain radios and towers

-

Compete on price against incumbents

This is asymmetric upside.

Amazon gets paid as long as DISH continues to generate traffic and pay its cloud bills, whether DISH is thriving or grinding through competitive pressure, while DISH only truly wins if its margins survive scale.

If DISH’s economics deteriorate to the point of distress, however, Amazon also risks losing a significant future cloud and distribution customer.

Why DISH Accepts the Deal

This is not naïveté; it is constraint-driven strategy.

DISH faces:

-

Capital scarcity

-

FCC build-out timelines

-

The need to launch quickly

Cloud-native architecture and Amazon distribution offer:

-

Speed to market

-

Reduced upfront spend

-

National reach without retail stores

For a challenger, these trade-offs are rational.

But they are survival tactics, not power plays.

The MVNO Reality Behind “Fourth Carrier”

Despite “fourth carrier” language, DISH still relies heavily on roaming and MVNO agreements with incumbents like AT&T and T-Mobile.

Operationally, this means:

-

Traffic routing decisions are dynamic

-

Cost per subscriber varies by location

-

Native network utilization remains uneven

Labeling DISH as a symmetric peer to Verizon obscures the hybrid reality.

The Cloud-Native Margin Trap

Cloud-native telecom is excellent at starting networks. It may be unproven at finishing them at very large scale.

At national scale, several pressures can emerge:

- Per‑GB costs can start to dominate architecture elegance

- Latency optimization can become expensive

- Cloud pricing power can tilt toward the provider

Traditional carriers amortize CAPEX over decades.

Cloud carriers rent compute indefinitely.

The question more analysts are starting to ask is:

At 50 million subscribers, who is more likely to have better margins—the operator or the cloud vendor?

Counterarguments — and Why They Fall Short

Counterargument 1: “Amazon Will Eventually Bundle Wireless with Prime”

Rebuttal:

Bundling only makes sense when Amazon controls pricing and margins. Wireless pricing is regulated, competitive, and politically sensitive. Amazon gains more by staying upstream and optional.

Counterargument 2: “Cloud Costs Will Drop Over Time”

Rebuttal:

Cloud prices fall in some areas, rise in others, and always retain vendor leverage. Carriers cannot pause traffic to renegotiate pricing.

Counterargument 3: “Amazon Needs Wireless for Ecosystem Lock-In”

Rebuttal:

Amazon already controls the ecosystem layers that matter: identity, payments, devices, logistics, and cloud. Owning radios adds risk, not leverage.

Taken together, these counterarguments reveal a consistent pattern: most assumptions about the DISH Amazon wireless carrier story rely on intent rather than incentives. Amazon’s actions make sense only when viewed through control, cost, and risk allocation—not speculation about market entry. Understanding this distinction is essential before evaluating what the partnership actually changes in the wireless ecosystem.

Before moving on, it helps to separate the headlines from the mechanics. The table below contrasts common claims about the DISH Amazon wireless carrier story with how control, risk, and revenue actually operate.

The Strategic Pattern

A useful way to view Amazon’s behavior is that it rarely enters hard industries directly. It surrounds them.

It did not become:

- A movie theater chain → it became the distribution platform

- A trucking company → it became the logistics orchestrator

- Wireless appears to fit the same pattern.

What Experienced Readers Should Watch Instead

Ignore headlines about “Amazon Wireless.” Watch:

-

% of DISH traffic on native radios

-

AWS cost per subscriber over time

-

Margin trajectory as scale increases

-

Renegotiation leverage in cloud contracts

These determine whether DISH becomes a sustainable operator—or a long-term tenant.

Conclusion

So, Is DISH an Amazon Wireless Carrier?

No — and that distinction matters.

DISH is the wireless operator. Amazon is not. But DISH’s carrier role originally came into focus when it stepped in as the Department of Justice’s preferred fourth facilities‑based carrier during the T‑Mobile–Sprint merger process, taking over prepaid assets like Boost Mobile and spectrum to preserve competition.

Amazon, by contrast, does not operate radios or hold consumer wireless spectrum licenses in this arrangement.

Through cloud infrastructure and distribution, Amazon earns recurring revenue while largely avoiding direct exposure to:

- Spectrum risk

- Network reliability obligations

- Regulatory compliance as a carrier

- Subscriber churn management

That is why the DISH Amazon wireless carrier story is often misunderstood. The real shift is not Amazon entering telecom — it’s telecom operators increasingly operating on Amazon’s terms.

Earlier spectrum and prepaid‑asset deals that enabled DISH to sell wireless service under its own name while building a standalone 5G network set the stage for this newer, cloud‑heavy model.

The strategic conclusions in this article should be read as informed analysis based on current public information, not as statements of established fact.

For DISH, this relationship enables speed and survival. For Amazon, it enables scale without ownership.

Public filings describe DISH’s wireless segment and spectrum holdings in detail in its Form 10‑K with the U.S. Securities and Exchange Commission. Readers who want more background on next‑generation networks can also explore your overview of 5G technology to understand the broader technical context.

The real question going forward isn’t “Will Amazon become a wireless carrier?”

It’s “How many carriers can afford not to run on Amazon’s infrastructure?

FAQ —“DISH Amazon WIRELESS CARRIER”

These are written to directly match People Also Ask queries, support rich results, and reinforce topical authority.

Is DISH an Amazon wireless carrier?

No. DISH is an independent wireless carrier that owns spectrum and operates its own network. Amazon does not operate the network or own wireless spectrum; it provides cloud infrastructure and acts as a distribution channel.

Is Amazon becoming a wireless carrier with DISH?

There is no evidence that Amazon plans to become a wireless carrier. Amazon avoids owning regulated, capital-intensive infrastructure and instead benefits by supporting carriers through cloud services and retail distribution.

What is Amazon’s role in the DISH wireless network?

Amazon provides cloud infrastructure through AWS and sells certain DISH wireless plans on its retail platform. Amazon does not manage radio networks, spectrum, or customer service.

Does Amazon control DISH’s wireless network?

Amazon does not control DISH’s radios or spectrum, but DISH’s cloud-native 5G core relies heavily on AWS infrastructure. This creates operational dependency without transferring carrier ownership.

Why do articles say Amazon is entering wireless?

Many articles conflate Amazon’s cloud and retail involvement with network ownership. Selling plans or hosting network software is not the same as operating a wireless carrier.

Is DISH a full fourth wireless carrier in the US?

DISH is a hybrid operator. It operates its own 5G network in some areas but still relies on roaming and MVNO agreements with other carriers in regions where its coverage is limited.

Could Amazon bundle wireless service with Prime?

There is no confirmation of full Prime bundling. While discounted promotions are possible, deep bundling would expose Amazon to regulatory and margin risks it historically avoids.

Who benefits more from the DISH–Amazon relationship?

Amazon benefits from recurring cloud and distribution revenue with minimal risk. DISH benefits from faster rollout and lower upfront costs but faces long-term margin pressure as traffic scales.

Disclosure

This content has been prepared based on available technology industry analysis, operator disclosures, and infrastructure economics. AI assistance was utilized to compile, structure, and clarify complex telecom and cloud-architecture concepts for informed readers.